Want to save time reading a long and complicated SOC 2 Report? If you’re one of hundreds of organizations who need to quickly review a SOC 2 Report to help you make informed decisions, then this is the blog for you. Regulators, auditors, B2B partners and vendors use a SOC 2 report to conduct due diligence, review information security, and evaluate if an organization meets governance, risk, and compliance program requirements. This blog delves into the intricacies of SOC 2 reports, sheds light on where you will find critical information about the controls tested during the SOC 2 audit, and demystifies the SOC 2 Examination process.

What is a SOC 2 Report?

A SOC 2 Report is issued to an organization that has successfully undergone a SOC 2 Audit conducted by a CPA authorized and licensed by the AICPA. The validity of a CPA’s license can be verified at CPAverify.org. Although commonly referred to as a SOC 2 Certificate, the official term for the process of obtaining a SOC 2 Report is a SOC 2 Examination.

An organization undergoes a SOC 2 Audit during a SOC 2 Examination and gets a SOC 2 Report. A SOC 2 Audit evaluates if the organization meets the benchmarks of the Trust Service Criteria (TSCs) and Principles of the AICPA. Although all SOC 2 audit firms adhere to the AICPA-defined procedures for conducting SOC 2 audits, the format and output of the reports vary. Each SOC 2 firm uses its own template to issue the SOC 2 report. Therefore, it is crucial for the organization receiving the report to review it objectively.

Many organizations opt to acquire System and Organization Control (SOC) 2 reports to share comprehensive insights and assure customers about the controls within their service organization. These reports focus on the Trust Services Criteria: Security, Availability, Processing Integrity, Confidentiality, and Privacy. While SOC 1 and SOC 3 reports are also pursued, SOC 2 reports have widespread recognition and adoption across industries.

Additionally, SOC 2 reports are tailored to various systems utilized by customers and companies. By encompassing controls addressing specific requirements such as disaster recovery solutions and security risk monitoring, they provide a more in-depth analysis of organizational systems than SOC 1 and SOC 3 reports.

During a SOC 2 Examination (often called a SOC 2 Certification), organizations have the option to obtain either a Type 1 or Type 2 report or both. For organizations that have previously documented controls through an automation partner, Type 1 reports can be expedited. These reports, known as point-in-time assessments, evaluate the design of controls on a specific date. Conversely, Type 2 reports undergo auditing over 3 to 12 months.

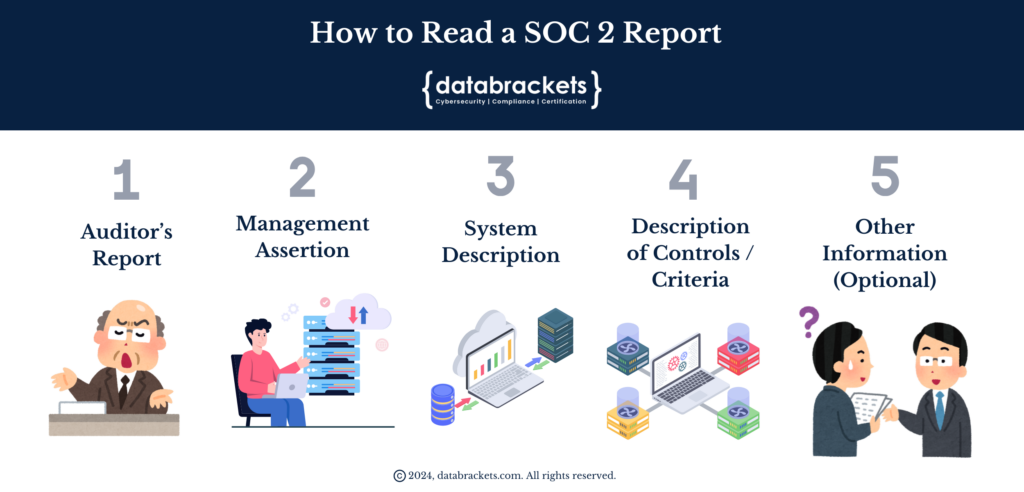

SOC 2 reports provide assurance to current and prospective customers, demonstrating the presence of robust procedures and controls aimed at delivering safe and reliable services. While SOC 2 auditors don’t have a fixed format for issuing a SOC 2 Report, there are generally five main sections based on the AICPA’s guidelines.

Auditor’s Report

Management Assertion

System Description

Description of Controls or Criteria

Other Information (optional)

Section 1: Auditor’s Report

When navigating a SOC 2 report, the Auditor’s Report serves as your initial guide. Auditors format the report to state their opinion from the outset clearly. Stakeholders typically refer to this opinion first to gauge whether there are any issues and their level of severity. This section presents the auditor’s assessment, which can be divided into four potential opinions: qualified, unqualified, adverse, or disclaimer. This section is likely one of the most important for SOC 2 report readers, as it provides a summary of the security control design, implementation, and test results directly and succinctly.

Qualified Opinion

Although the term “qualified” might typically imply a positive outcome, within the context of SOC 2 reports, it denotes that the auditor has identified at least one area where operations didn’t meet optimal standards during the reporting period. While this may initially raise some concerns, it’s important to recognize that encountering a qualified opinion isn’t an insurmountable obstacle. It’s quite common for auditors to uncover issues indicating either ineffective design or operation of controls. You need to review if the controls that didn’t meet requirements are critical for your organization and if the vendor can share a deadline to meet the benchmarks.

Unqualified Opinion

Conversely, receiving an unqualified opinion signifies that the organization has successfully met the requirements. This rating represents the highest level attainable for a SOC 2 report, signaling that the auditor did not detect any deficiencies in the effectiveness of security controls during the specified reporting period.

Adverse Opinion

Auditors render an adverse opinion when they detect widespread shortcomings and conclude that users cannot trust the service organization’s systems within the defined scope. As a reader of a SOC 2 Report, if you see an Adverse opinion, you have 2 options:

a) Decide to stop working with the vendor

b) Dive deeper into the reason behind this opinion & if any remediation measures were undertaken after the report was issued. You can request the evidence documents to prove the effectiveness of their remediation efforts as well.

Disclaimer of Opinion

If auditors lack adequate evidence to formulate an opinion, they issue a disclaimer of opinion. In such a case, the organization needs to gather additional evidence of their controls to undergo another audit.

Section 2: Management Assertion

This section focuses on how the organization prepared and implemented its system descriptions. Consider this section as the formal oath-taking of the service organization, confirming that all information provided to auditors is truthful and comprehensive to the best of their knowledge and capability. It’s an overview stating that:

The controls stated in the Management Assertion were designed and implemented by the organization within a specific reporting period. This is critical for the auditor.

The security controls in the description operated effectively throughout the specified reporting period (SOC 2 Type 2 only).

While this section doesn’t contain technicalities, it acts as a precursor to the next section, where the organization describes its system descriptions in greater detail. Organizations that work with an experienced SOC 2 Compliance Readiness Partner can receive support in drafting this section since it is submitted by them.

Section 3: System Description

After the management’s assertion, the organization shares important information regarding the people, processes, and technology that supports their product or service. These descriptions offer a panoramic view of their organizational systems and regulatory measures covering all aspects of the services offered, the kind of data they work with, hold or transmit, and the type of users. They share an overview of the internal functioning of their organization, the systems used to deliver their services, the locations of employees and teams, etc. The insights provided herein aid auditors in evaluating the efficacy of the system’s components in safeguarding customer data.

Here are the eight components that the AICPA recommends for this section:

Types of services rendered

Principal service commitments and system requirements

Components of the system

Trust services criteria and their corresponding controls

Complementary user entity controls

Complementary subservice organization controls

Records of System incidents

Significant changes to the system during the reporting period

Frequently, the organization undergoing a SOC 2 audit may not include the relevant system in the scope of the system description. It is important for SOC 2 report readers to verify that the systems they plan to use are included in the system description.

Section 4: Description of Controls or Criteria

Section 4 of the SOC 2 report is the most comprehensive segment, offering a detailed account of the functioning of an organization’s security controls. The description of controls or criteria is the most important section to read while evaluating vendors and partners before entrusting them with your data. This is where test results are shared (after testing security controls during the SOC 2 audit period), and you can gauge the efficacy and suitability of working with the vendor or partner. However, before you review this section, you need to find the information about the controls that are within the scope of the audit. The auditor only tests controls that are within the scope of the audit.

Depending on the report you request, Type 1 and Type 2 reports appear relatively the same for the first three sections. However, differences between the reports are significant in this section. A SOC 2 Type 1 Audit assesses whether the controls are designed effectively, and a SOC 2 Type 2 Audit assesses whether they are also functioning at an optimal level.

Type 1 Report

Since Type 1 reports are a point-in-time assessment, this section of the SOC 2 report includes a list of tested controls without the auditor’s test results. It focuses on the suitability of the control architecture. Under the AICPA, Type 1 reports only require the auditor’s evaluation if the controls were designed correctly within a specific period of time.

Type 2 Report

Type 2 reports, on the other hand, include all the controls tested along with the auditor’s test results. This includes only the controls that are in the scope, and that may be 60-80 controls. The auditor issues a similar opinion as SOC 2 Type 1 with the addition of operating effectiveness, and this is critical for you to judge their effectiveness. The controls are tested over a period of time, typically a 3–12-month period. These test results are the primary consideration behind the opinion given by the auditor. Most stakeholders and potential B2B customers often refer to this section when reviewing a SOC 2 Type 2 report. In this section, you can find any security control the auditor might have flagged as operating ineffectively.

Auditors may test controls through one of three methods – inquiry, inspection, or observation. Inquiring about controls may not meet your objectives, and you need to evaluate if they have also used evidence-based documentation. Inspecting controls involves examining evidence that they function optimally during the audit period. This leads to the highest level of confidence. Alternatively, if the auditor uses observation, they will monitor evidence of controls like a third party by providing sample customer contracts. However, observation can only be used if the cloud environment is proprietary. After testing controls, auditors make a note of exceptions in a matrix-like presentation. SOC 2 report readers should pay close attention to the controls where exceptions are noted and thoroughly examine the details of these exceptions.

Response by Management

If the auditor identifies exceptions while testing security controls, the organization is given a platform to share its response. Management plays a crucial role in this process, including their response in either this section or the next, which is optional. Their response provides a detailed context for the specific control(s) that were not functioning optimally. In some instances, an exception may be noted for a control that is not applicable; for example, if an organization solely uses the cloud for data storage and processing, the physical security of devices is not applicable. In such cases, management may justify not securing devices, highlighting their active involvement in the audit process. In addition to reviewing the management response section of the SOC 2 report, readers are advised to request documented updates on the latest remediation status for each exception noted in the report.

Section 5: Other Information (optional)

Section 5, is a flexible component within a SOC 2 report, empowering the organization to provide additional details about their SOC 2 audit. It can be included with Section 4 or as a separate section, giving the auditor the freedom to structure the report. Within this segment, you can delve into the responses to any exceptions uncovered in the SOC 2 Type 2 Report. For instance, if the auditor identifies a particular deficiency in Section 4, this segment allows the organization to offer further context and reasons behind the existence of such gaps, ensuring you have all the information you need at your fingertips to make a decision.

Getting a SOC 2 Bridge Letter

SOC 2 Reports are valid for 12 months and organizations need to undergo another SOC 2 Audit to prove they are SOC 2 Compliant for the next 12 months. B2B partners who request a SOC 2 Report, often make the continuity of their contracts contingent on SOC 2 Compliance. However, at times, they may have a gap between the validity of their SOC 2 Reports for 1-2 months. To maintain these business partnerships, the organization and their B2B partners have the option of requesting the CPA firm to issue a ‘SOC 2 Bridge Letter’. This letter attests that during those months, their controls appeared to be in place. This is an important concept and document while making an informed decision about a vendor.

Key Takeaways

A SOC 2 report is designed to communicate how an organization manages controls related to trust services, and its value lies in understanding what was actually tested rather than assuming certification implies blanket security assurance.

The report’s scope defines which systems, services, and trust criteria are covered, making scope review essential to determine whether the assessment aligns with your specific risk or vendor evaluation needs.

Understanding the distinction between Type I and Type II reports is critical, because one reflects control design at a point in time while the other evaluates operational effectiveness over a defined period.

The auditor’s opinion provides high-level insight into control performance, but it should be read alongside detailed testing results to understand the nature and impact of any exceptions.

Control descriptions explain how the organization claims controls operate, which must be evaluated for clarity, relevance, and alignment with the services being relied upon.

Testing results reveal whether controls functioned as intended during the assessment period, offering practical insight into consistency and reliability rather than theoretical design.

Exceptions and deviations require careful interpretation, as their severity depends on frequency, scope, and relevance to the services or data you depend on.

Complementary user entity controls identify responsibilities that fall on the customer rather than the service provider, highlighting shared accountability that is often overlooked.

A SOC 2 report should be treated as a decision-support document, informing risk assessment and vendor management rather than serving as a simple pass-fail artifact.

databrackets as your SOC 2 Compliance Readiness Partner

Typically, organizations tend to directly look for a licensed CPA firm and sign up for a SOC 2 Audit. There are several stumbling blocks in this approach and it can lead to superfluous payments that can be avoided. When you approach a licensed CPA, you will not receive guidance on which type of report you need (SOC 1, SOC 2 or SOC 3) or the Trust Services Criteria and security controls for your industry. They are not required to help clients with guidance to implement or prove their SOC 2 Compliance. Their mandate is to conduct an impartial audit and issue a structured report to help your clients understand if your systems are secure.

Working with a SOC 2 Compliance Readiness Partner can help you save a significant amount of time, money and resources. Our security experts have extensive experience working with clients across industries with the sole purpose of helping to position your organization for a successful audit. The tasks that we undertake, as your SOC 2 Compliance Readiness Partner includes:

Initial Consultation and Scoping

Educating the Client

Gap Analysis

Control Mapping

Documentation Review and Development

Remediation Planning

Implementation Support

Internal Audit

Readiness Assessment Report

Ongoing Support and Monitoring

The data of our SOC 2 Readiness clients is maintained in a structured format on our GRC platform – dbACE and is accessible to the CPA that you chose to work with. You can refer to the controls, Trust Services Criteria and the 2 sections of your SOC 2 Report which you need to submit – the Management’ Assertion and a Description of your System, using your unique login. We also collaborate with certified CPA firms whom you can chose to work with, if you decide to do so. Hence, working with a Readiness Partner helps you to not only prepare for SOC 2 Certification but also ensures that your security controls are implemented adequately and you have evidence to prove their effectiveness.

Overview of databrackets

Our team of security experts has supported organizations across a wide variety of industries to align their processes with security frameworks like HIPAA, 21 CFR Part 11, ISO 27001:2022, SOC 2, NIST SP 800-53, NIST Cybersecurity Framework, NIST SP 800-171, GDPR, CMMC etc.

We are constantly expanding our library of assessments and services to serve organizations across industries. Schedule a Consultation if you would like to Connect with an Expert to understand how we can customize our services to meet your specific requirements.

Summary

To summarize,

A SOC 2 report is a detailed assurance document meant to explain how an organization’s controls support trust services criteria, and its usefulness depends on careful interpretation rather than assuming it represents blanket security certification.

The scope section establishes which systems, services, and trust criteria were examined, making it essential to confirm that the assessment actually covers the areas relevant to your risk, data, or reliance on the service provider.

The distinction between Type I and Type II reports shapes how conclusions should be drawn, since one evaluates control design at a single point in time while the other assesses whether controls operated effectively over a defined period.

The auditor’s opinion offers a high-level assessment outcome, but meaningful insight comes from reading beyond the opinion to understand what was tested and how results were achieved.

Control descriptions provide context on how the organization says its controls function, helping readers assess whether those controls reasonably address the risks associated with the services provided.

Testing procedures and results reveal how consistently controls operated during the assessment window, offering evidence of reliability rather than theoretical compliance.

Exceptions must be evaluated in context, as their significance depends on frequency, scope, and relevance to the specific risks you are trying to manage.

Complementary user entity controls clarify responsibilities that customers must fulfill, reinforcing that security assurance is shared rather than fully transferred to the service provider.

A SOC 2 report is best used as a risk evaluation tool that informs vendor due diligence and trust decisions, not as a simple pass-or-fail compliance artifact.